DALBERGIA Market Update | Q4 2025

From the UK Government Autumn Budget to inflation and interest rates- we break down what’s currently shaping the sector.

Read the full report below.

DALBERGIA Market Update | Q4 2025

From the UK Government Autumn Budget to inflation and interest rates- we break down what’s currently shaping the sector.

Read the full report below.

UK GOVERMENT AUTUMN BUDGET

Costs continue to rise across the construction industry, particularly for SMEs, so the announcement to pause the land fill tax reform will be strongly welcomed. This policy reversal should help ease cost pressures in the residential and infrastructure sectors, as cost effective waste management can continue to exist. In addition, the £1.5bn fund to support training will also ease cost pressures and may encourage companies to hire. Overtime, this could eventually alleviate the ongoing labour shortages. This is an ongoing concern with the ONS reporting that the UK construction workforce has decreased to its lowest number in nearly 25 years in 3Q2025 to 2,054,009 workers. However the increase in minimum wage, along with the delay in increasing the National Insurance threshold, will place additional financial strain on the construction industry by increasing their overheads. Furthermore, the introduction of road tax on EVs could significantly impact companies that have transitioned their fleets to EVs/ Hybrids, adding further pressure to their operating costs.

UK CONSTRUCTION INSIGHT

BCIS (Nov 2025) reported new orders are up by29.3% from the same time last year, with public housing and private industrial being the main increasing sectors. However, compared to 2Q2025,new orders in private housing, infrastructure, and public work are all down.

Even with an increase in new orders, BCIS are still reporting significantly lower material deliveries than pre pandemic levels, indicating that the UK construction industry has not fully recovered. Brick and concrete block deliveries are 27.4% and 21.3%lower respectively in October 2025 than pre pandemic levels. This trend extends to ready mixed concrete deliveries too, which are 30% lower in 3Q2025 than they were pre pandemic.

BSR approvals are improving, with 578 applications now having been decided within the 12 week period nearly halving the legacy cases. However, the BSR are still going to fall behind with an average of 48decisions made per week, but with 50 new cases being added each week that leaves them with a 2application deficit per week.

INFLATION RATES

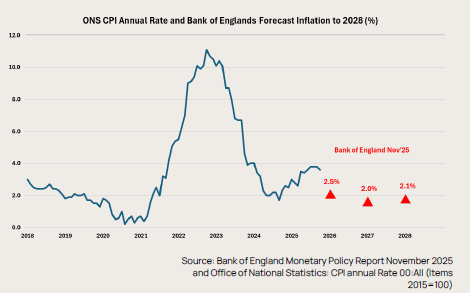

The Consumer Price Index shows that the inflation rate has remained above the 2% target in October 2025,at 3.6%.

Inflation has decreased from 3.8% for the first time in 5 months due to a lower rise in gas and electricity prices and Ofgem’s price cap compared to last year. There has also been a decrease in hotel prices but food prices continue to increase. The Bank of England is forecasting that Inflation rates will return to their target rate of 2% by 2027.

INTEREST RATES

UK interest rates have maintained the current

rate of 4.0% in November 2025.

With the inflation rate decreasing the market

is anticipating that the December 2025 Bank

of England decision on interest rates will be to

cut the rate further from 4% to 3.75%.

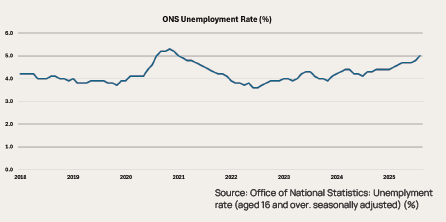

Unemployment has risen to a 3 year high of

5%, and job vacancies have fell to 723,000

between August and October 2025 (ONS).

This, combined with a slowdown in wage

growth from 5% to 4.8%, indicates a

weakening in labour-market tightness. As a

result, a less constrained labour market

reduces employers’ need to offer higher

wages to attract staff, thereby easing wage

driven inflationary pressures.